How do Certificates of Deposits Work?

Have extra funds or savings you won't need for a long period? Then, it might be ideal to put your excess money in a certificate of deposits (CDs) account. Are Certificates of Deposit accounts better than money market and savings accounts? Well, that depends on your financial situation.

While Certificates of Deposits offer more rates than other types of accounts like savings and money market accounts, you'll have to lock your funds in the account for a fixed period. The compounded interest and principal would be paid after the time elapses. Early withdrawal would result in a penalty fee. Learn more about the Difference between Savings and Checking accounts.

What Exactly is a Certificate of Deposits?

A certificate of deposits, or share certificate, refers to a special type of savings account offered by credit unions and banks. They usually come with higher rates but would require you to lock your funds for a fixed period. Check out these best savings accounts and interest rates.

Because of this distinct feature of CDs, they are considered a long-term savings option. Returns are guaranteed unlike investing in stocks. The only drawback with CDs is that withdrawing the money you deposited early would attract a penalty fee.

In this article, we will be sharing with you everything you need to know about CDs and suggest some other alternatives worth considering.

How Do Certificates of Deposits Work?

Below is the breakdown of the concepts of a certificate of deposits account.

Rates

CDs earn the same rate over time, unlike normal savings accounts. It could be advantageous in a scenario where you've locked your funds when the rates are high, then later see a drop in rates across the board.

However, this can also mean you'll be at a disadvantage when rates rise above the locked value.

Terms

To open a CD, you need to decide how long you want your funds locked in the account. The typical time range varies from 3 months to 5 years. This affects the amount of the early withdrawal penalty fee as well as the rates you get from the CD.

As a rule of thumb, know that the longer the time, the higher the rate, and the higher the penalty fee.

Safety

CDs, like other bank accounts, are covered by federal deposit insurance for up to $250,000 at FDIC-insured banks and the NCUA-insured credit unions. If a financial organization goes bankrupt, you are assured to get your money back.

Maturity date

CDs have a specific date of maturity. This could be months or years depending on the agreed terms when opening the account. You can automate the renewal of your CDs with many banks, however, you should consider if it's going to be in your best interest before making that choice.

Penalty

Withdrawing funds from a CD before its maturity date would incur a penalty fee. The amount charged can range from several months to a year's worth of interest depending on the financial institution.

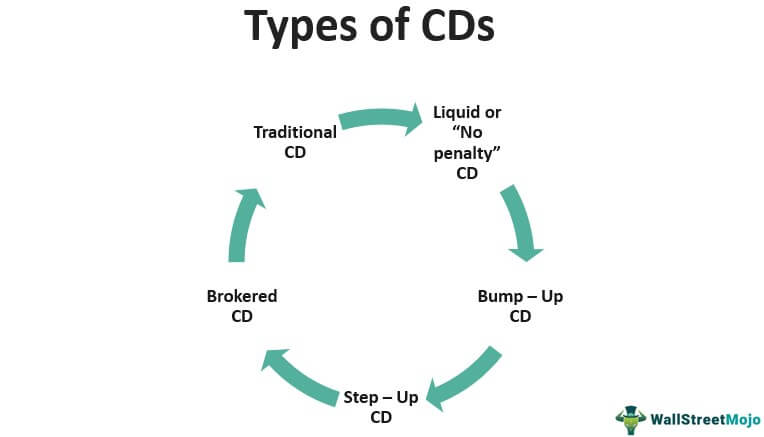

Types of CDs

Credit unions and banks offer multiple CD options, each having its pros and cons. Here're some of the CD types you'll find in most financial institutions:

1. No penalty or Liquid CDs

With liquid CDs, there's no restriction on early withdrawals and you won't incur any charge for doing so. You can capitalize on this flexibility to relocate your funds into a higher-paying CD when the opportunity arises.

The drawback of this type of CD is that they offer lower interest rates than regular CDs.

2. Bump-up CDs

You'll get similar benefits to liquid CDs when you open bump-up CDs. It's possible to exit a low-interest yielding CD for a higher-rate one. But in this case, your previous CD account is maintained when relocating to the higher rate.

3. Step-up CDs

You're not bound to the rate that was in place when you opened your CD because these types of CDs come with a regularly scheduled increase in interest rates. The increment could be once every six or seven months.

4. Brokered CDs

You can purchase brokered CDs through a brokerage account. Instead of opening a bank account and using their CD selection, you can acquire brokered CDs from a variety of issuers and keep them all in one location. While this gives you some flexibility, there are several risks to brokered CDs.

5. Traditional CDs

A Traditional CD lets you put in a specific amount of money for a fixed period while getting a determined interest rate. You can cash out at the end of the term or keep the CD for another term. Early withdrawal can lead to high penalties, and they can eat away at your earnings and even your principal sum. Thes fees are made known to you when you open the account. Always calculate your interest before opening a Traditional CD.

6. Jumbo CDs

Jumbo CDs are characterized by extremely high minimum balance requirements. The average required by most financial institutions is an excess of $100,000. Your locked funds are secured due to the $250,000 safety net provided by federal deposit insurance in credit unions and banks.

They also offer a much higher interest rate than regular CDs. If you have large funds you won't miss for a long time, this can be an ideal option for you.

7. Zero-Coupon CD

Zero-coupon CDs, let you purchase the CD at a lower price than its "par value," which is how much it will be worth on maturity. "Coupon" is a term for payment of interest at a set time.

"Zero-coupon" implies that there is no interest to be paid. For instance, with $50,000, you could buy a 10-year, $100,000 CD that pays 0% interest for 10 years. You'd get the $100,000 face value of the CD when it's over, as well as the interest that's accrued.

When you buy zero-coupon CDs, they are often long-term investments and you don't get any money until the CD is over, which is a major disadvantage, in our opinion.

Also, each year, you're given a "phantom" money that you don't have. This is another disadvantage that means you won't be getting any money, but you'll have to pay taxes on the money you make.

This is simply a bigger tax base with each year. Before going into this option, make sure you can pay your taxes. See the 10 Best Tax Software for you

Foreign Currency CD

The foreign currency CD is not meant for people who are new to investing or who are afraid of taking risks. They are hard to understand. You can make them in Dollars, British pounds, euros, and other currencies. You can buy them with US dollars and get them back in dollars on the maturity of the CD. For this type of CD, there is no guarantee that you will get your interest on time because payment is made with foreign currency.

Investing in Foreign currency CD may give you higher returns, but currencies and global economic conditions can change, which makes them a riskier investment.

It's also possible to lose money when you convert the foreign currency CD back to dollars, though. A strong dollar can slash your profit or even make you lose money.

This type of CD may not be FDIC-insured, so it may not be worth much money. To get FDIC insurance, the amount you invest must be backed by the bank that issued it.

FDIC says that If the principal sum is at risk of being lost, other than for an early withdrawal penalty, then the product is not covered by the FDIC should the bank fail.

When to Open a CD

A CD could be an excellent strategy to save money if you have excess money that you wish to keep safe for a few months or years. The early-withdrawal penalty on a CD will also help you curb the habit of dipping your hands in your savings.

The concept of how interest rates work with CDs is that the rates increase with term length. A three-month CD would pay you a relatively lower interest rate than 12-month CDs.

On average, the most common periods provided by most financial institutions on CDs are usually three, six, twelve, twenty-four, or sixty months max.

A word of caution: Avoid creating a CD account that has a too lengthy maturation date. You don't want your money to be locked up when you need it, especially when withdrawing it early can cost you money.

When Not to Open a CD

There are several reasons why you should not deposit your money in a CD despite being a helpful savings tool in some situations. Most of the time, whether a CD is good for you depends on some external market factors as well as your financial requirements.

In today's interest rate climate, some high-yield savings accounts pay higher interest rates than CDs. Opting for a standard savings account with no time constraints on withdrawals might be a better option. As a plus, you'll be able to earn greater interest from these accounts.

Another factor you should consider is inflation. Ensure to compare your CD's interest rate to the current rate of inflation. There have been some cases where inflation rates exceed levels higher than CD interest rates over time.

When this happens, it's not wise to keep your money tied down in a CD account. You'll end up losing value on your money which defeats the purpose of locking your funds in the first place.

Finally, the early-withdrawal penalty charged when you remove your funds before the maturity date is perhaps the largest disadvantage of a CD. The early withdrawal penalties are not to be taken lightly as they can be very costly so consider your options thoroughly.

How to Choose a CD?

When selecting a CD, there are several variables to consider. First and foremost, when do you require the funds? Consider CDs with a shorter time if you need them right now. However, if you're saving for a five-year goal, go for a CD with a longer-term and greater interest rate.

Take into account the current economic situation. CD laddering can be a wise strategy if interest rates appear to be rising or if you wish to open many CDs.

Top CD Strategies

Here're some of the creative ways you can maximize your CD accounts:

1. CD Laddering

CD laddering is a strategy where you diversify your funds into numerous CDs with varying terms. Re-invest the money from matured CDs into a new long-term CD to take advantage of greater rates that can potentially be offered in the future.

2. CD Barbell

CD barbell and CD laddering are similar in many ways but they're two different strategies entirely. Here, you diversify your money into short-term and long-term CDs to wait for better rates before investing entirely in long-term CDs.

3. CD Bulleting

Having multiple CDs with a similar maturity date forms the basis of a CD bulleting strategy. The big idea is to save for large purchase years in the future, such as a down payment on a house.

Ways to Utilize CDs in your savings Portfolio

Decide the purpose for saving your money

In some cases, a savings account or money market account might be better than a CD. When you save on a fixed-rate CD, you know exactly how much money you'll make during the term. if you want to grow your money quickly or for a long time, it will be advisable to look into other types of investments.

Options like stocks, mutual funds, exchange-traded funds (ETFs), or index funds may be able to make more money, but you also have greater chances of losing your money.

Consider the amount needed to be liquid.

For short-term funds, think about putting them in a CD. Putting your money in an easy account like a savings or money market account is a good idea for the cash going you intend to use soon, for purchases and emergencies.

You usually get better rates with Long-term CDs. However, it is hard to find many CDs with more than 2 years that are paying much more in interest than shorter-term CDs.

Search and find the best deal.

To get a good CD deal, you need to put in the work. Make sure to look at what your current bank is offering, and then compare it to what different CDs are paying. Find a bank that has rates that are much higher than what is the obtainable national average.

When you've done that, look online for the best rates with regard to the terms you intend to use. Other types of banks pay less compared to online banks because the online banks are not saddled with a lot of charges like brick and mortar banks, hence higher payouts.

They also need your deposits, and the only way to attract you is by giving you a higher rate of return. Note that credit unions are not-for-profit groups, so, their CD rates are lower.

Make sure the terms of the CD is understandable to you.

Be aware that a CD isn't the best place to keep the money that you need until the expiration of the term. Taking your money out of a CD earlier than stipulated may make you ensure a penalty for early withdrawal, which could mean losing the money you earned and also your principal sum.

You may need a savings account or another type of account if you are putting emergency funds or you will likely need your money before the CD term is up.

Take note of the promotion terms or bonus rates of the CDs

Some Credit Unions and local banks may give incentives and special rates that are usually only available to people who deposit a lot of money. People who live in certain counties, towns, or regions may be able to get CDs with very good interest rates from their local banks. Read also The Difference between Banks and Credit Unions

The standard rates at the institution will give you a sense of how competitive CD rates will be when the time comes for CD renewal.

Steer clear of automatic rollovers.

Even if you had a promotional rate, you should check your CD again when it's about to run out, because it might renew at a bad rate. Most initial CD terms come at a good rate, but the same can't be said for renewal

Figure out when your funds will be needed.

When you figure out when you'll need your money, you can avoid paying fees early. CD terms usually last from 3 months to 6 years or longer. If you intend to invest in real estate, a one-year CD might be a good investment. a protect your money and also get a good rate of return.

You can put a part of your emergency fund in CD and also in a savings account if you have a large fund. The one in a savings account can be used for emergencies.

A lot of people invest money that they won't need for at least five years in things like stocks and mutual funds. But those strategies don't guarantee that the money will be worth more at the end of the day.

If you don't want to lose your money, CDs are a good choice. Consumers who open a CD at an FDIC-insured bank can be sure that their money is safe. FDIC: Each depositor at an FDIC-insured bank is protected to at least $250,000 per insured bank.

Alternatives to Certificates of Deposits

Here are some other savings options worth exploring apart from CDs:

1. Opening a High-yield savings account

If you prefer having the freedom to withdraw your deposit when needed, opening a high-yield savings account might be a better option for you. Some online banks offer competitive rates up to 0.75%.

See some examples of online banks that offer high-interest rates.

2. Short-term bond funds

You can loan your money to the government or a business in form of a bond. They also produce higher yields than a regular savings account and are generally safe. However, like any other type of investment, short-term bonds have their risks.

3. U.S savings bonds

This type of savings option is for people with really long-term goals like saving up for marriage or college. Your funds are mostly secure in a savings bond. Also, you can open a Treasury inflation-protected security (TIPS) bond which can help you beat inflation.

CD vs. savings account

You can't make additional contributions to a certificate of deposit because it locks your money away for a certain duration and rate. CDs feature higher interest rates than conventional savings accounts in exchange for the loss of access.

On the other hand, a normal savings account offers additional flexibility, allowing you to deposit funds at any time and withdraw funds at least once each month.

CD vs. bond

CDs are federally insured savings accounts with a term of up to five years. You normally have to pay a penalty if you withdraw early.

https://bit.ly/3ux5TKB

Comments

Post a Comment